VectorBT Pro - Aligning MTF time series Data with Resampling

Software Requirements : vectorbtpro, python3

Resampling of the market data is needed for strategies that involve multiple time frames, often referred to as “top down analysis” or “Multi Time Frame (MTF) analysis”. There are two types of resampling, called upsampling and downsampling.

Before thinking of upsampling and downsampling time-series data, let's use the analogy of an UltraHD (4K) television to better understand these terms intuitively. When you feed a 1080p video source to a 4K TV it will Upsample the pixels, giving you a high resolution image. Essentially, you will get a high granularity (finer, hi-res image) from a low granularity (coarse, low-res image). The opposite ( downsampling ) happens when you play a 4K video file on an old 📺 HD TV.

In the context of time series data,

Example: 15 Minute Data → 1 Hour Data

Example : 1 Hour Data → 15 Minute Data

In multi-time frame strategy analysis, we have to deal with the problem of integrating time series data (eg: close price) from multiple time frames.

To make our data-analytics and back-testing simulation process easier, we usually like to have a single time-series dataframe ( mtf_df ) which contains all the values from whatever time-frames we require (eg: 5m, 15min, 1h. 4h, 1D, 1W etc.) . This MTF dataframe will have a base-line frequency which will typically be the highest frequency (i.e highest granularity or the lowest timeframe time-series data, eg: 5m ) with which you want to do your signal generation for the strategy. The process of creating this MTF dataframe with resampled data is called Alignment.

In alignment, we basically merge the MTF time-series resampled data into a single dataframe using ffill() and shift() operations. This is very easily done using vbt.resampler() objects and using those resampler objects as an argument in vbt.resample_opening() function for open price and vbt.resample_closing() when dealing with close, high, low prices and indicators.

Loading and Resampling Data

Loading the data using vbt.HDF functionality of the 1-minute granularity

## Import Required Libaries

import vectorbtpro as vbt

import pandas as pd

## Load m1 data

m1_data = vbt.HDFData.fetch('../data/GU_OHLCV_3Y.h5')

m1_data.wrapper.index #pandas doaesn't recognise the frequency because of missing timestamps

Output:

DatetimeIndex(['2019-08-27 00:00:00+00:00', '2019-08-27 00:01:00+00:00',

'2019-08-27 00:02:00+00:00', '2019-08-27 00:03:00+00:00',

'2019-08-27 00:04:00+00:00', '2019-08-27 00:05:00+00:00',

'2019-08-27 00:06:00+00:00', '2019-08-27 00:07:00+00:00',

'2019-08-27 00:08:00+00:00', '2019-08-27 00:09:00+00:00',

...

'2022-08-26 16:50:00+00:00', '2022-08-26 16:51:00+00:00',

'2022-08-26 16:52:00+00:00', '2022-08-26 16:53:00+00:00',

'2022-08-26 16:54:00+00:00', '2022-08-26 16:55:00+00:00',

'2022-08-26 16:56:00+00:00', '2022-08-26 16:57:00+00:00',

'2022-08-26 16:58:00+00:00', '2022-08-26 16:59:00+00:00'],

dtype='datetime64[ns, UTC]', name='time', length=1122468, freq=None)

Resampling (Downsampling) the Data from 1 Minute Timeframe / Granularity to other Timeframes/Granularities.

- Converting 1 Minute (

M1) to 15 Minute (M15)- Converting 1 Minute (

M1) to 1 Hour (H1)- Converting 1 Minute (

M1) to 4 Hours (H4)

This resampling uses the vbt.resample() method for the downsampling operations, after which we see the frequency is identified correctly as 15T (15 mins)

m15_data = m1_data.resample('15T')

h1_data = m1_data.resample("1h")

h4_data = m1_data.resample('4h')

print(m15_data.wrapper.index)

Output:

DatetimeIndex(['2019-08-27 00:00:00+00:00', '2019-08-27 00:15:00+00:00',

'2019-08-27 00:30:00+00:00', '2019-08-27 00:45:00+00:00',

'2019-08-27 01:00:00+00:00', '2019-08-27 01:15:00+00:00',

'2019-08-27 01:30:00+00:00', '2019-08-27 01:45:00+00:00',

'2019-08-27 02:00:00+00:00', '2019-08-27 02:15:00+00:00',

...

'2022-08-26 14:30:00+00:00', '2022-08-26 14:45:00+00:00',

'2022-08-26 15:00:00+00:00', '2022-08-26 15:15:00+00:00',

'2022-08-26 15:30:00+00:00', '2022-08-26 15:45:00+00:00',

'2022-08-26 16:00:00+00:00', '2022-08-26 16:15:00+00:00',

'2022-08-26 16:30:00+00:00', '2022-08-26 16:45:00+00:00'],

dtype='datetime64[ns, UTC]', name='time', length=105188, freq='15T')

resample() method was used in the above operation, is it pandas or vbt.resample() ?If the object you are resampling is of class

vbt then the numba-compiled resample() function of VectorBT will be used automatically. If the resampled object is a pandas.Series or pandas.DataFrame then the pandas resample() method will be used automatically.As seen in the code below the respective (OHLC) can be obtained using the .get() method.

# Obtain all the closing prices using the .get() method

m15_close = m15_data.get()['Close']

## h1 data

h1_open = h1_data.get()['Open']

h1_close = h1_data.get()['Close']

h1_high = h1_data.get()['High']

h1_low = h1_data.get()['Low']

## h4 data

h4_open = h4_data.get()['Open']

h4_close = h4_data.get()['Close']

h4_high = h4_data.get()['High']

h4_low = h4_data.get()['Low']

OR, you can can also simply follow the pandas convention like resampled_data.column_name to retrieve the column data

# Obtain all the closing prices using the .get() method

m15_close = m15_data.close

## h1 data

h1_open = h1_data.open

h1_close = h1_data.close

h1_high = h1_data.high

h1_low = h1_data.low

## h4 data

h4_open = h4_data.open

h4_close = h4_data.close

h4_high = h4_data.high

h4_low = h4_data.low

The OHLC for both the H4 4-Hourly Candle Data as well as the closing price for the 15m Candle Data was obtained.

Multi-Time Frame Indicator Creation

VectorBT has a built-in method called vbt.talib() which calls the required indicator from talib library and runs it on the specified time-series data (Eg: Close Price or another indicator). We will now create the following indicators (manually) on the M15, H1 and H4 timeframes using the :

RSIof 21 periodBBANDSBolllinger BandsBBANDS_RSIBollinger Bands on the RSI

rsi_period = 21

## 15m indicators

m15_rsi = vbt.talib("RSI", timeperiod = rsi_period).run(m15_close, skipna=True).real.ffill()

m15_bbands = vbt.talib("BBANDS").run(m15_close, skipna=True)

m15_bbands_rsi = vbt.talib("BBANDS").run(m15_rsi, skipna=True)

## h4 indicators

h1_rsi = vbt.talib("RSI", timeperiod = rsi_period).run(h1_close, skipna=True).real.ffill()

h1_bbands = vbt.talib("BBANDS").run(h1_close, skipna=True)

h1_bbands_rsi = vbt.talib("BBANDS").run(h1_rsi, skipna=True)

## h4 indicators

h4_rsi = vbt.talib("RSI", timeperiod = rsi_period).run(h4_close, skipna=True).real.ffill()

h4_bbands = vbt.talib("BBANDS").run(h4_close, skipna=True)

h4_bbands_rsi = vbt.talib("BBANDS").run(h4_rsi, skipna=True)

When talib() creates the RSI indicator time-series, it is known to create it with NaNs (null-values), so it is a good idea to run ffill(), forward filling operation to fill the missing values. On this note, it is also a good idea in general, to investigate the talib results and compare it with the original time-series data (Close Price) for abnormal number of NaN values and then decide on ffill() operation

We will now initialize the empty dict called data and fill it with key - value pairs of the 15m time-series data.

## Initialize dictionary

data = {}

col_values = [

m15_close, m15_rsi, m15_bbands.upperband, m15_bbands.middleband, m15_bbands.lowerband,

m15_bbands_rsi.upperband, m15_bbands_rsi.middleband, m15_bbands_rsi.lowerband

]

col_keys = [

"m15_close", "m15_rsi", "m15_bband_price_upper", "m15_bband_price_middle", "m15_bband_price_lower",

"m15_bband_rsi_upper", "m15_bband_rsi_middle", "m15_bband_rsi_lower"

]

# Assign key, value pairs for method of time series data to store in data dict

for key, time_series in zip(col_keys, col_values):

data[key] = time_series.ffill()

Alternative (One-Liner) Method of Indicator Creation

VectorBT also offers a more convenient one-liner method of creating this multi-time frame indicators

rsi_period = 21

rsi = vbt.talib("RSI", timeperiod=rsi_period).run(

m15_data.get("Close"),

timeframe=["15T", "1H" , "4H"],

skipna=True,

broadcast_kwargs=dict(wrapper_kwargs=dict(freq="15T"))

).real

bbands_price = vbt.talib("BBANDS").run(

m15_data.get("Close"),

timeframe=["15T", "1H", "4H"],

skipna=True,

broadcast_kwargs=dict(wrapper_kwargs=dict(freq="15T"))

)

bbands_rsi = vbt.talib("BBANDS").run(

rsi,

timeframe=vbt.Default(["15T", "1H" ,"4H"]),

skipna=True,

per_column=True,

broadcast_kwargs=dict(wrapper_kwargs=dict(freq="15T"))

)

Note : The method of indicator creation shown above using talib('IndicatorName').run with broadcast_kwargs argument automatically does the ffill() operation. This one liner method doesn't resample to 15T only because of broadcast_kwargs argument, in fact, using broadcast_kwargs we just provide vbt with the true frequency of your data in case this frequency cannot be inferred from data. Without specifying it the method will still work (we will just get a warning if frequency cannot be inferred)

So here we we specify the broadcast_kwargs argument, because m15_data.get("Close") contains gaps and pandas cannot infer its frequency as 15T, this approach works only because of the timeframe argument and because indicators always return outputs of the same index as their inputs, such that we're forced to resample it back to the original frequency. If pandas can infer the frequency of the input series, we don't need to specify broadcast_kwargs argument at all.

## Initialize dictionary

data = {}

## Assign key, value pairs for method 2 of Automated One-liner MTF indicator creation method

col_values = [

[m15_close.ffill(), rsi['15T'], bbands_price['15T'].upperband, bbands_price['15T'].middleband, bbands_price['15T'].lowerband, bbands_rsi['15T'].upperband, bbands_rsi['15T'].middleband, bbands_rsi['15T'].lowerband],

[rsi['1H'], bbands_price['1H'].upperband, bbands_price['1H'].middleband, bbands_price['1H'].lowerband, bbands_rsi['1H'].upperband, bbands_rsi['1H'].middleband, bbands_rsi['1H'].lowerband],

[rsi['4H'], bbands_price['4H'].upperband, bbands_price['4H'].middleband, bbands_price['4H'].lowerband, bbands_rsi['4H'].upperband, bbands_rsi['4H'].middleband, bbands_rsi['4H'].lowerband]

]

col_keys = [

["m15_close", "m15_rsi", "m15_bband_price_upper", "m15_bband_price_middle", "m15_bband_price_lower", "m15_bband_rsi_upper", "m15_bband_rsi_middle", "m15_bband_rsi_lower"],

["h1_rsi", "h1_bband_price_upper", "h1_bband_price_middle", "h1_bband_price_lower", "h1_bband_rsi_upper", "h1_bband_rsi_middle", "h1_bband_rsi_lower"],

["h4_rsi", "h4_bband_price_upper", "h4_bband_price_middle", "h4_bband_price_lower", "h4_bband_rsi_upper", "h4_bband_rsi_middle", "h4_bband_rsi_lower" ],

]

## Assign key, value pairs for method 2 of Automated One-liner MTF indicator creation method

for lst_series, lst_keys in zip(col_values, col_keys):

for key, time_series in zip(lst_keys, lst_series):

data[key] = time_series

Alignment & Up-sampling

Let's now see what is resampler in VectorBT. Resampler is an instance of the Resampler class, which simply stores a source index and frequency, and a target index and frequency. The vbt.resampler() method can just work with the source index and target index and can automatically infer the source and target frequency. In contrast to Pandas, vectorbt can also accept an arbitrary target index for resampling

Resampler(

source_index,

target_index,

source_freq=None,

target_freq=None,

silence_warnings=None

)

where the arguments, are

source_index : is index_like, Index being resampled.

target_index : is index_like ,Index resulted from resampling.

source_freq : frequency_like or bool, Frequency or date offset of the source index. Set to False to force-set the frequency to None.

target_freq : frequency_like or bool, Frequency or date offset of the target index. Set to False to force-set the frequency to None.

silence_warnings : bool, Whether to silence all warnings.

We will now create a custom function called create_resamplers() using this vbt.Resampler() function to create a resampler object to convert H4 time-series

def create_resamplers(result_dict_keys_list : list, source_indices : list,

source_frequencies :list, target_index : pd.Series, target_freq : str):

"""

Creates a dictionary of vbtpro resampler objects.

Parameters

==========

result_dict_keys_list : list, list of strings, which are keys of the output dictionary

source_indices : list, list of pd.time series objects of the higher timeframes

source_frequencies : list(str), which are short form representation of time series order. Eg:["1D", "4h"]

target_index : pd.Series, target time series for the resampler objects

target_freq : str, target time frequency for the resampler objects

Returns

===========

resamplers_dict : dict, vbt pro resampler objects

"""

resamplers = []

for si, sf in zip(source_indices, source_frequencies):

resamplers.append(vbt.Resampler(source_index = si, target_index = target_index,

source_freq = sf, target_freq = target_freq))

return dict(zip(result_dict_keys_list, resamplers))

Using this function we can create a dictionary of vbt.Resampler objecters stored by appropriately named keys.

## Create Resampler Objects for upsampling

src_indices = [h1_close.index, h4_close.index]

src_frequencies = ["1H","4H"]

resampler_dict_keys = ["h1_m15","h4_m15"]

list_resamplers = create_resamplers(resampler_dict_keys, src_indices, src_frequencies, m15_close.index, "15T")

print(list_resamplers)

Output:

{'h1_m15': <vectorbtpro.base.resampling.base.Resampler at 0x16c83de70>,

'h4_m15': <vectorbtpro.base.resampling.base.Resampler at 0x16c5478e0>}

The output shows that two vbt.Resampler class objects have been created in memory.

The resample_closing() and resample_opening() operations don't require any ffill() operations and they automatically align the source time-series data to the target frequency, which in our case is 15T (15 mins)

## Add H1 OLH data - No need to do ffill() on resample_closing as it already does that by default

data["h1_open"] = h4_open.vbt.resample_opening(list_resamplers['h1_m15'])

## Add H4 OLH data - No need to do ffill() on resample_closing as it already does that by default

data["h4_open"] = h4_open.vbt.resample_opening(list_resamplers['h4_m15'])

We use resample_opening only if information in the array happens exactly at the beginning of the bar (such as open price), and resample_closing if information happens after that (such as high, low, and close price). You can see the effect of this resample_opening operation with the print() statements below:

print(h4_open.info()) ## Before resampling pandas series

<class 'pandas.core.series.Series'>

DatetimeIndex: 6575 entries, 2019-08-27 00:00:00+00:00 to 2022-08-26 16:00:00+00:00

Freq: 4H

Series name: Open

Non-Null Count Dtype

-------------- -----

4841 non-null float64

dtypes: float64(1)

memory usage: 102.7 KB

None

print(data["h4_open"].info()) ## After resampling pandas series

<class 'pandas.core.series.Series'>

DatetimeIndex: 105188 entries, 2019-08-27 00:00:00+00:00 to 2022-08-26 16:45:00+00:00

Freq: 15T

Series name: Open

Non-Null Count Dtype

-------------- -----

105188 non-null float64

dtypes: float64(1)

memory usage: 1.6 MB

None

## Use along with Manual indicator creation method for MTF

series_to_resample = [

[h1_high, h1_low, h1_close, h1_rsi,

h1_bbands.upperband, h1_bbands.middleband, h1_bbands.lowerband,

h1_bbands_rsi.upperband, h1_bbands_rsi.middleband, h1_bbands_rsi.lowerband],

[h4_high, h4_low, h4_close, h4_rsi,

h4_bbands.upperband, h4_bbands.middleband, h4_bbands.lowerband,

h4_bbands_rsi.upperband, h4_bbands_rsi.middleband, h4_bbands_rsi.lowerband]

]

data_keys = [

["h1_high", "h1_low", "h1_close", "h1_rsi",

"h1_bband_price_upper", "h1_bband_price_middle","h1_bband_price_lower",

"h1_bband_rsi_upper", "h1_bband_rsi_middle", "h1_bband_rsi_lower"],

["h4_high", "h4_low", "h4_close", "h4_rsi",

"h4_bband_price_upper", "h4_bband_price_middle", "h4_bband_price_lower",

"h4_bband_rsi_upper", "h4_bband_rsi_middle", "h4_bband_rsi_lower"]

]

## Create resampled time series data aligned to base line frequency (15min)

for lst_series, lst_keys, resampler in zip(series_to_resample, data_keys, resampler_dict_keys):

for key, time_series in zip(lst_keys, lst_series):

resampled_time_series = time_series.vbt.resample_closing(list_resamplers[resampler])

data[key] = resampled_time_series

Alignment and Resampling when using one-liner method of indicator creation

In this method, we have already dealt with resampling and aligning the indicators, so all we have to do is just resample the open and closing prices of the respective timeframes required.

## Resample prices to match base_line frequency (`15T`)

series_to_resample = [

[h1_open, h1_high, h1_low, h1_close],

[h4_open, h4_high, h4_low, h4_close]

]

data_keys = [

["h1_open", "h1_high", "h1_low", "h1_close"],

["h4_open", "h4_high", "h4_low" ,"h4_close"]

]

## Create resampled time series data aligned to base line frequency (15min)

for lst_series, lst_keys, resampler in zip(series_to_resample, data_keys, resampler_dict_keys):

for key, time_series in zip(lst_keys, lst_series):

if key.lower().endswith('open'):

print(f'Resampling {key} differently using vbt.resample_opening using "{resampler}" resampler')

resampled_time_series = time_series.vbt.resample_opening(list_resamplers[resampler])

else:

resampled_time_series = time_series.vbt.resample_closing(list_resamplers[resampler])

data[key] = resampled_time_series

Creating The Master DataFrame

Now that we have resampled the various time series to the different timeframes, created and run our indicators, we can finally create the composite mtf_df dataframe from this data which is properly aligned to the baseline frequency (in our case 15T) that will allow us to properly create the Buy/Long and Sell/Short conditions for whichever MTF (Multi Time Frame) Strategy that we indend to backtest.

cols_order = ['m15_close', 'm15_rsi', 'm15_bband_price_upper','m15_bband_price_middle', 'm15_bband_price_lower',

'm15_bband_rsi_upper','m15_bband_rsi_middle', 'm15_bband_rsi_lower',

'h1_open', 'h1_high', 'h1_low', 'h1_close', 'h1_rsi',

'h1_bband_price_upper', 'h1_bband_price_middle', 'h1_bband_price_lower',

'h1_bband_rsi_upper', 'h1_bband_rsi_middle', 'h1_bband_rsi_lower',

'h4_open', 'h4_high', 'h4_low', 'h4_close', 'h4_rsi',

'h4_bband_price_upper', 'h4_bband_price_middle', 'h4_bband_price_lower',

'h4_bband_rsi_upper', 'h4_bband_rsi_middle', 'h4_bband_rsi_lower'

]

## construct a multi-timeframe dataframe

mtf_df = pd.DataFrame(data)[cols_order]

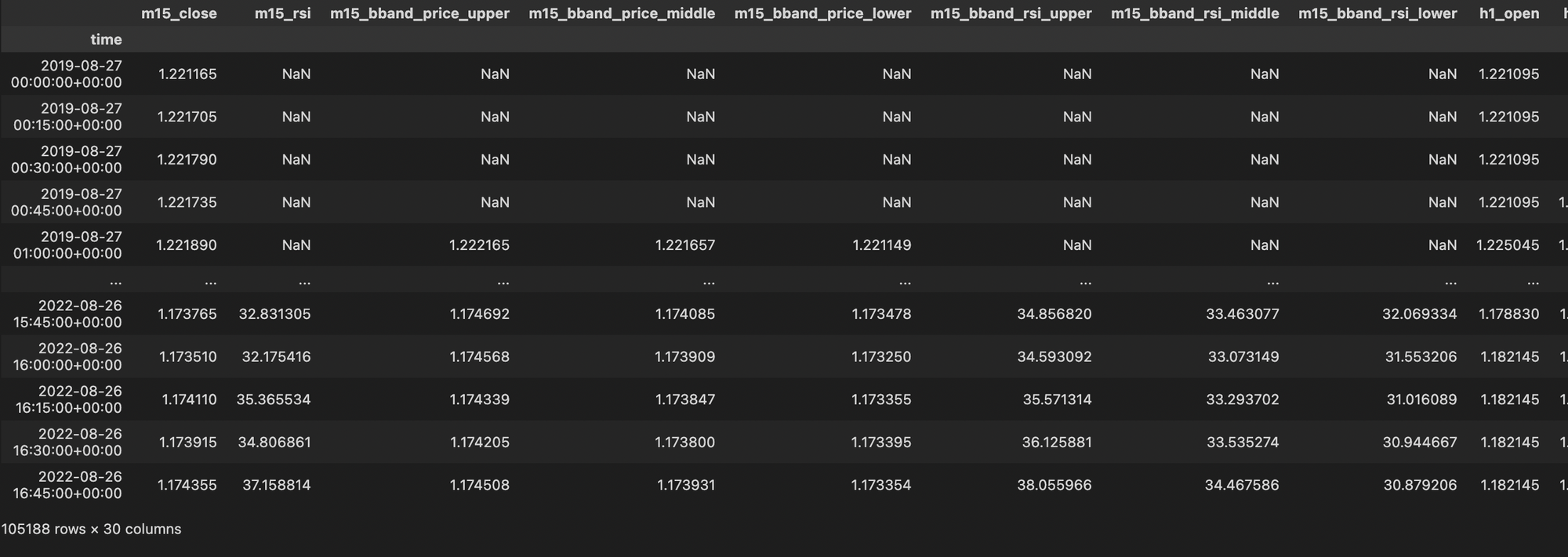

display(mtf_df)

The mtf_df multi-time frame master dataframe will have the following columns each of which will help us define the logic of the strategy.

m15_close: 15 Minute Closing Pricem15_rsi: RSI values on them15closing price of period 21m15_bband_price_upper: The upper bollinger band onm15closing pricem15_bband_price_middle: The middle bollinger band onm15closing pricem15_bband_price_lower: The lower bollinger band onm15closing pricem15_bband_rsi_upper: The Upper Bollinger Band on theM15RSI Valuesm15_bband_rsi_middle: The Middle Bollinger Band on theM15RSI Valuesm15_bband_rsi_lower: The Lower Bollinger band on theM15RSI Valuesh1_open: The opening price of theH1candleh1_high: The High Price of theH1Candleh1_low: The Low Price of theH1Candleh1_close: The Closing Price of theH1Candleh1_rsi: RSI Values on theH1closing price of period 21h1_bband_price_upper: The Upper Bollinger Band OnH1Closing Priceh1_bband_price_middle: The Middle Bollinger Band OnH1Closing Priceh1_bband_price_lower:The Lower Bollinger Band OnH1Closing Priceh1_bband_rsi_upper: The Upper Bollinger Band on theH1RSI Valueh1_bband_rsi_middle: The Middle Bollinger Band on theH1RSI Valueh1_bband_rsi_lower: The Lower Bollinger Band on theH1RSI Valueh4_open: The opening price of theH4candleh4_high: The High Price of theH4Candleh4_low: The Low Price of theH4Candleh4_close: The Closing Price of theH4Candleh4_rsi: RSI Values on theH4closing price of period 21h4_bband_price_upper: The Upper Bollinger Band OnH4Closing Priceh4_bband_price_middle: The Middle Bollinger Band OnH4Closing Priceh4_bband_price_lower:The Lower Bollinger Band OnH4Closing Priceh4_bband_rsi_upper: The Upper Bollinger Band on theH4RSI Valueh4_bband_rsi_middle: The Middle Bollinger Band on theH4RSI Valueh4_bband_rsi_lower: The Lower Bollinger Band on theH4RSI Value

print(mtf_df.info())

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 105188 entries, 2019-08-27 00:00:00+00:00 to 2022-08-26 16:45:00+00:00

Freq: 15T

Data columns (total 33 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 m15_close 105188 non-null float64

1 m15_rsi 105167 non-null float64

2 m15_bband_price_upper 105184 non-null float64

3 m15_bband_price_middle 105184 non-null float64

4 m15_bband_price_lower 105184 non-null float64

5 m15_bband_rsi_upper 105163 non-null float64

6 m15_bband_rsi_middle 105163 non-null float64

7 m15_bband_rsi_lower 105163 non-null float64

8 h1_open 105188 non-null float64

9 h1_high 105185 non-null float64

10 h1_low 105185 non-null float64

11 h1_close 105185 non-null float64

12 h1_rsi 105101 non-null float64

13 h1_bband_price_upper 105169 non-null float64

14 h1_bband_price_middle 105169 non-null float64

15 h1_bband_price_lower 105169 non-null float64

16 h1_bband_rsi_upper 105085 non-null float64

17 h1_bband_rsi_middle 105085 non-null float64

18 h1_bband_rsi_lower 105085 non-null float64

19 h4_open 105188 non-null float64

20 h4_high 105173 non-null float64

21 h4_low 105173 non-null float64

22 h4_close 105173 non-null float64

23 h4_rsi 104837 non-null float64

24 h4_bband_price_upper 105109 non-null float64

25 h4_bband_price_middle 105109 non-null float64

26 h4_bband_price_lower 105109 non-null float64

27 h4_bband_rsi_upper 104773 non-null float64

28 h4_bband_rsi_middle 104773 non-null float64

...

32 signal 105188 non-null int64

dtypes: bool(2), float64(30), int64(1)

memory usage: 29.9 MB

Summary

In general, the resampling and alignment steps for creating a multi-time frame (MTF) dataframe can be summarized in the below diagram.

- We start with the highest granularity of OHLCV data possible (1m) and then downsample the data to higher timeframes (5m, 15m, 1h, 4h etc.)

- We then create the indicators on the multiple time frames required but at this juncture we don't forward fill the price data. After the indicator is created we can

ffill()the resulting series if we are going with the manual method of indicator creation. - In order to create the composite, merged MTF dataframe we employ

resample_opening()on the open price orresample_closing()on every other time series, with the appropriatevbt.Resampler()objects, so that all the time-series are aligned to the base-line frequency time series.